In an era where financial security is paramount, life insurance remains one of the most reliable ways to protect loved ones from unexpected hardships. As of December 2025, the landscape of life insurance providers is competitive, with companies offering innovative digital applications, no-medical-exam options, and customizable coverage. SuperMoney’s life insurance review page serves as a valuable resource for consumers, aggregating user reviews, financial strength ratings, and key policy features to help shoppers compare top providers side by side.

SuperMoney’s platform emphasizes transparency, allowing users to explore thousands of consumer reviews for free. The site highlights providers based on factors like user recommendation scores (e.g., “Strongly recommended”), the number of reviews, death benefit ranges, term lengths, and financial strength ratings from agencies like AM Best. While results may be influenced by advertising partnerships—SuperMoney discloses that it receives compensation from some featured companies—the core rankings prioritize community feedback and objective data such as claims-paying ability and affordability.

Why Life Insurance Matters in 2025

Life insurance provides a financial safety net, replacing lost income, covering debts, or funding funeral expenses (typically $7,000–$10,000). For families with dependents, it’s essential; without it, survivors may face significant burdens. SuperMoney stresses that most people need term life for its affordability, while permanent policies suit those seeking lifelong coverage or cash value accumulation.

Key types include:

- Term Life: Temporary coverage (10–40 years) at low cost—ideal for young families.

- Whole Life: Lifelong protection with cash value growth and potential dividends.

- Universal Life: Flexible premiums and death benefits, often with investment components.

- Variable Universal: Ties cash value to market performance for higher growth potential (but riskier).

Factors influencing premiums: age, health, gender, tobacco use, and hobbies. Younger, healthier applicants secure the best rates. SuperMoney advises comparing quotes while noting details like underwriting class (Preferred Plus to Standard) and additional fees.

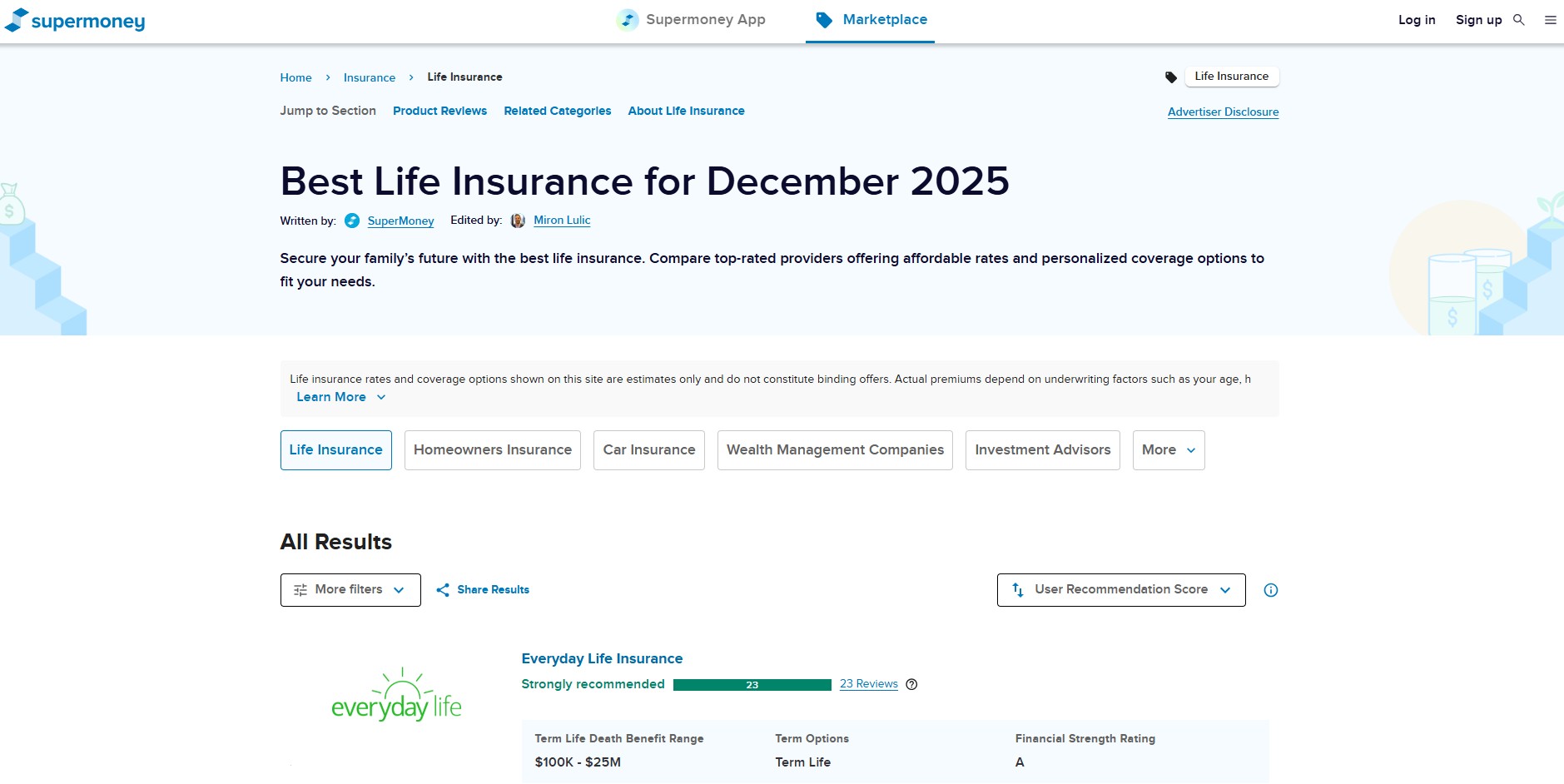

SuperMoney’s Top-Rated Life Insurance Providers for December 2025

SuperMoney’s December 2025 rankings feature providers excelling in user satisfaction and features. Many earn “Strongly recommended” status with high financial ratings (A or A+). Standouts include digital-first companies offering quick online applications and no-exam policies.

- Everyday Life Insurance (A-rated, 23 reviews): Starts at ~$4.61/month (average $15). Highlights include flexible payment dates and no medical exams. Uses AI-driven “Predictive Protection” for personalized quotes.

- Ladder Life Insurance (A-rated, 13 reviews): Fully digital, up to $3 million coverage without exams (for eligible applicants ages 20–60). Terms 10–30 years, starting ~$5/month. Allows easy coverage adjustments.

- New York Life (A++ rated, 9 reviews): Traditional powerhouse with no-exam options up to $1 million. Available nationwide, known for stability.

- Fabric Life Insurance (A+ rated, 20 reviews): Family-focused, seamless online process with tools like free wills.

- Lantern Life Insurance (A+ rated, 18 reviews): Excels in instant quotes and simplified issuance.

Other notables: Transamerica (A+), Sproutt (A+), Ethos (A-), Principal (A+), USAA (A+, military-affiliated), and Prudential (A+).

These rankings blend user votes (unbiased by compensation) with features like media filters and engagement metrics. SuperMoney notes pros (affordability, ease) outweigh cons (limited death benefits in some no-exam policies).

Cross-Referencing with Broader 2025 Industry Rankings

While SuperMoney focuses on user-driven and partner-highlighted providers, independent sources like Forbes, U.S. News, Bankrate, and J.D. Power provide complementary views. Common top performers in 2025 include:

- MassMutual: Often ranked #1 overall for low rates, dividends ($2.5 billion+ projected), and whole life options.

- State Farm: Tops customer satisfaction (J.D. Power leader), with strong term policies.

- Protective Life: Best for long terms (up to 40 years) and competitive pricing.

- Northwestern Mutual: Record dividends ($8.2 billion in 2025), superior financial strength (A++).

- Nationwide: Excellent no-exam and variety of policies.

- Pacific Life: Low term rates, high coverage limits.

Digital platforms like Ethos and Ladder align with SuperMoney’s emphasis on speed, while traditional giants like Guardian and Penn Mutual shine in permanent coverage and dividends.

How to Choose the Right Policy Using Tools Like SuperMoney

SuperMoney recommends:

- Determine coverage: 10–15x annual income, plus debts/funeral costs.

- Compare quotes: Record premium, term, rating, and underwriting details.

- Prioritize financial strength: A+ or better ensures claim payment.

- Read reviews: Check J.D. Power, NAIC complaints, and user feedback.

- Consider no-exam: Faster but higher premiums or lower limits.

Alternatives if unnecessary: Build emergency funds or invest in retirement accounts. For most, term suffices; permanent for estate planning or high-net-worth needs.

SuperMoney’s pros: Comprehensive comparisons, educational guides on types and costs. Cons: Potential ad influence on visibility, complex for beginners.

Final Thoughts: Securing Peace of Mind

In 2025, options abound—from Ladder and Ethos’ tech-driven simplicity to New York Life’s reliability. SuperMoney demystifies choices with data-backed tools, empowering informed decisions. Always verify quotes directly, as rates vary by personal factors. Life insurance isn’t just a policy—it’s legacy protection. Start comparing today for tailored coverage that fits your life stage and budget.